By this point, real estate developers and contractors know well the pain of procuring building materials in 2021. However, while we’ve taken a look at the rising (and falling) price of the materials themselves, a new report from Rider Levett Bucknall offers a comprehensive perspective at the actual costs of put-in-place construction in individual markets and how they compare to one another. It may not be a huge shocker to local builders, but the quarterly increase in Chicago area construction costs is significant.

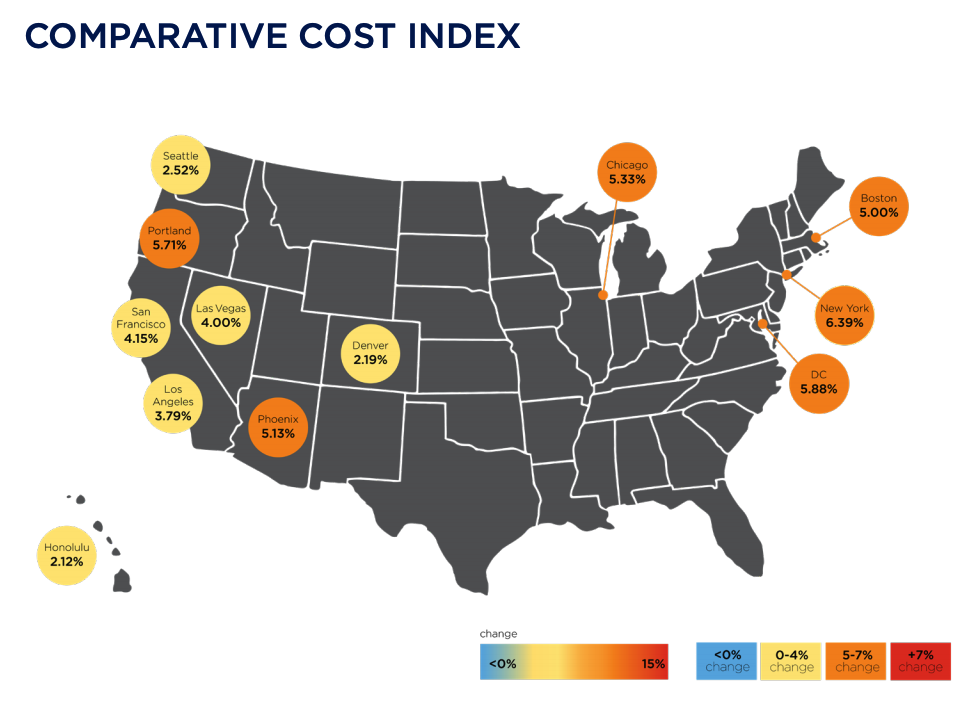

The annual change in the comparative cost index for Chicago is up by 5.33% from April 2020 to April 2021, the report indicates. While Chicago doesn’t lead the pack, it is still on the higher end of the spectrum when compared to small markets and the West Coast metros that are also highlighted. New York’s comparative cost index jumped 6.39% between April 2020 and April 2021 while Denver and Seattle were both at or just below 2.5%.

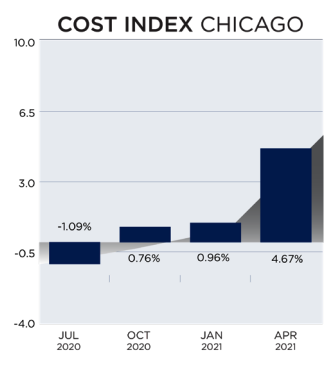

But when breaking the stats down further and viewing the individual market data by quarter, the numbers for Chicago appear a little more alarming. In this instance, Chicago does move up to the top of the list when viewing the quarterly change of 4.67% between Q1 and Q2 of 2021. Phoenix is in a close second place with a 4.29% increase in its cost index between Q1 and Q2 of this year while metros like Seattle, Denver, and Honolulu remained relatively flat quarter-over-quarter in the last year.

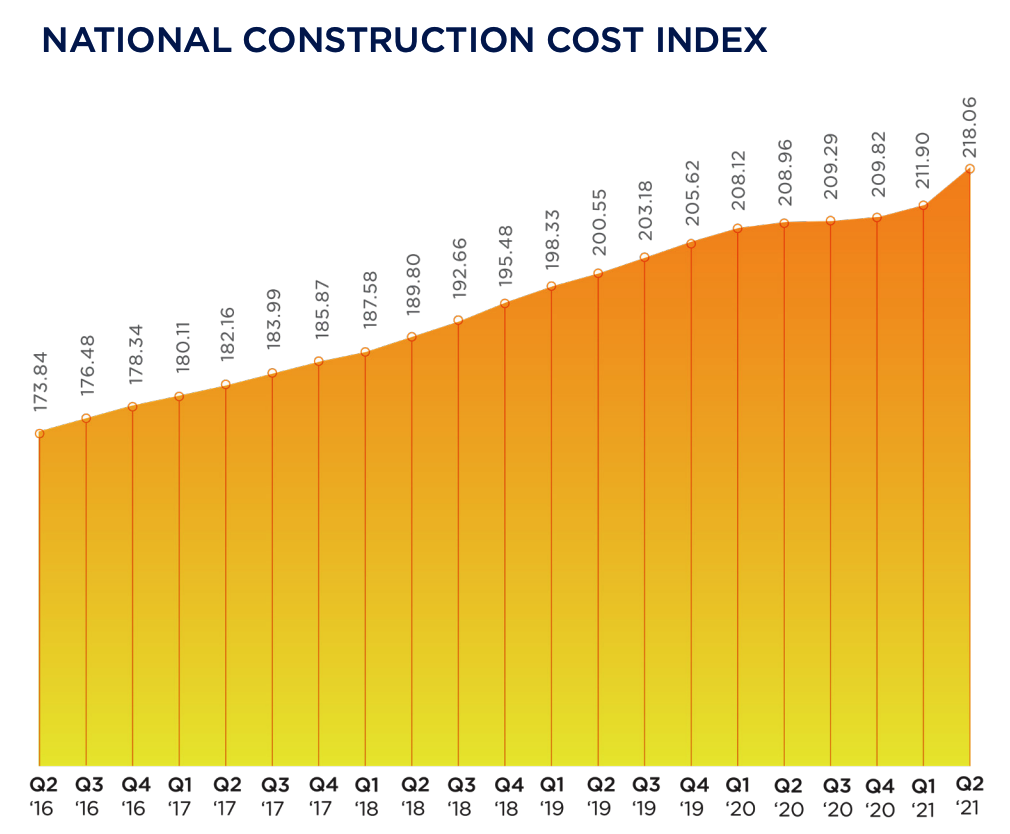

Now when zoom out and look at the national average, construction costs have steadily increased every quarter for the last several years. A chart in the report shows the national construction cost index at 173.84 points in Q2 2016 and has climbed to 218.06 in this last quarter. There was a very short plateau last year during the pandemic, but it picked back up substantially in the second quarter of this year.

The report also highlights the total investment in construction in recent months. The U.S. Department of Commerce predicts $1.524 billion worth of put-in-place construction for this April while the adjusted figure for March was $1.521 billion. Compare this to the $1.387 billion estimate for April 2020 and it’s clear to see how much more money has been spent on construction in recent months.

The rising costs come from high demand for materials, supply shortages and long lead times combined during a period of economic calamity, specifically high unemployment rates, protracted disruptions to businesses and inflation. However, the report does offer some good news with stats on a growing GDP, increasing consumer confidence and elevated architectural billings.