Towards the beginning of summer, it seemed that the increasingly lower COVID cases coupled with higher vaccination numbers provided enough hope that some business leaders were patiently waiting for in order to announce a return to the office. But as Labor Day approaches and cases are back on the rise, it’s really anyone’s guess as to what exactly will happen in the coming months in regards to the office market.

At least, this is what some CRE professionals in the office world are suggesting.

The office market has been deeply affected by the pandemic, and at this point, it’s still uncertain exactly when many employees could see a collective return to the downtown office environment. It’s more or less a “Lucy with the football” type of scenario, says Randy Waites, Principal and Managing Director of the Real Estate Management Services Group with Avison Young in Chicago.

“If you were to look at the end of May or early June, I think we all were thinking that Labor Day was quite a realistic possibility, and might have even been a little too far off,” Waites says of the situation. “[But now], I think that Labor Day is a stretch, frankly, from what I’m hearing across the country until people have a sense that the Delta variant is a little more under control.”

And while the Delta variant has led to a renewed indoor mask mandate in the city of Chicago, CRE professionals still believe that ultimately, employers will bring their teams back to the office eventually. It’s certainly a tough situation for all involved in office leasing and property management, but it’s one that will require further patience and resolve to get through.

“We’re a real estate company, we want a robust real estate market and we’ve pushed to have people come in to use our space as often as they can,” Waites says of his team’s effort to utilize their office space as much as possible. “It’s not doomsday or the death of the office and I think people worry about sending that message. It’s just more time was put back on the clock.”

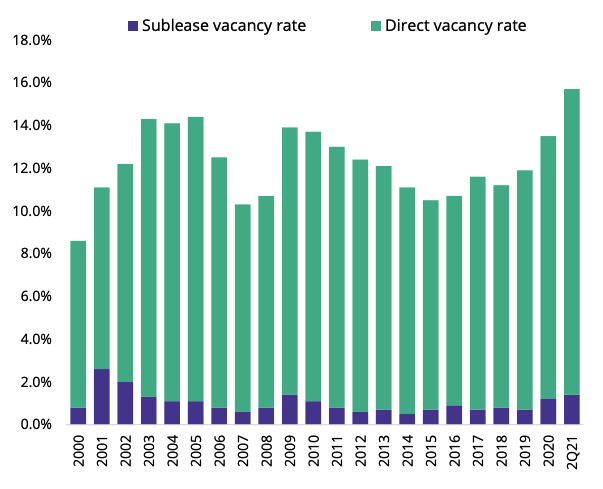

One indicator that has signaled continued troubles in the Chicago office market is the high level of available sublease space. The Chicago office market hit a record of available sublease space towards the end of 2020 when the metro region had just over 9 million square feet of office space for sublet, with nearly 6 million square feet of it in the city’s central business district.

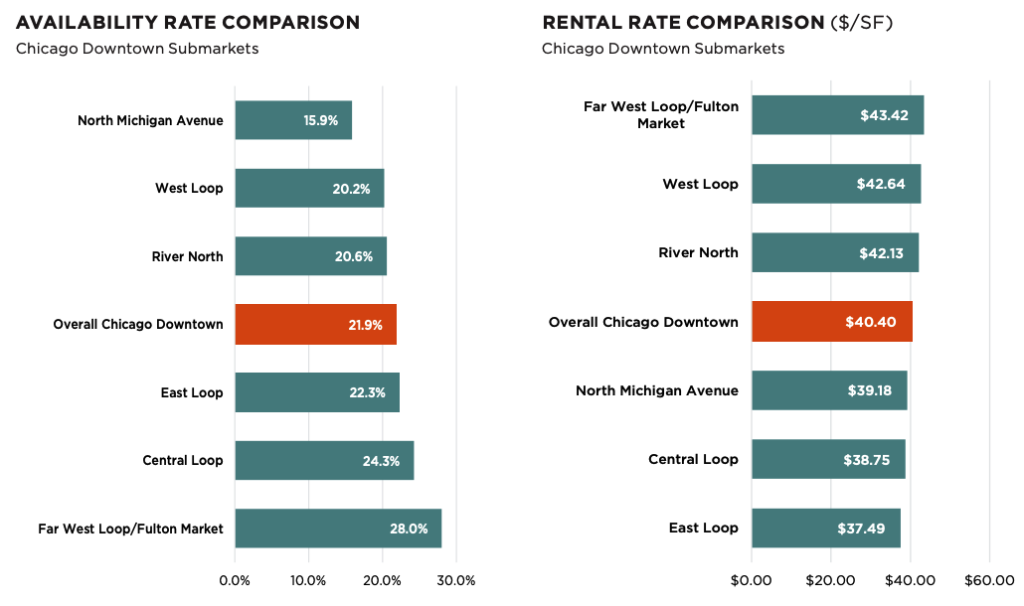

And recent reports are much the same. A June report from CBRE suggests that at a national level, Chicago is lagging many other major metros in its office recovery. The report indicates that the sublease market is still ample, with 88% more sublease space than there was at the pre-pandemic baseline. An Avison Young report for Q2 2021 puts the total sublet space in Chicago’s CBD at 5.4 million square feet, more or less unchanged from the previous quarter.

However, a report from London-based Savills shows the downtown sublet market still holding steady with the record 6 million square feet of available space. And in the suburbs, the overall level of all available office space increased in the second quarter to just over 31%, or just around four percent higher than in the same period during 2020.

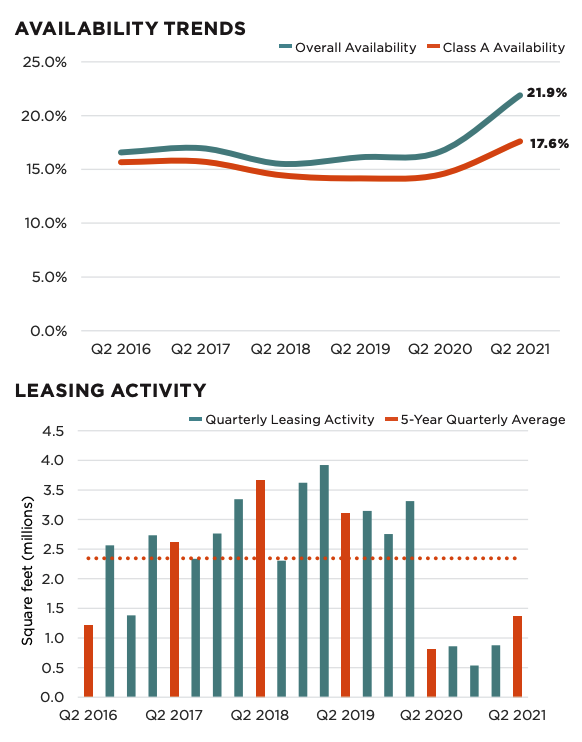

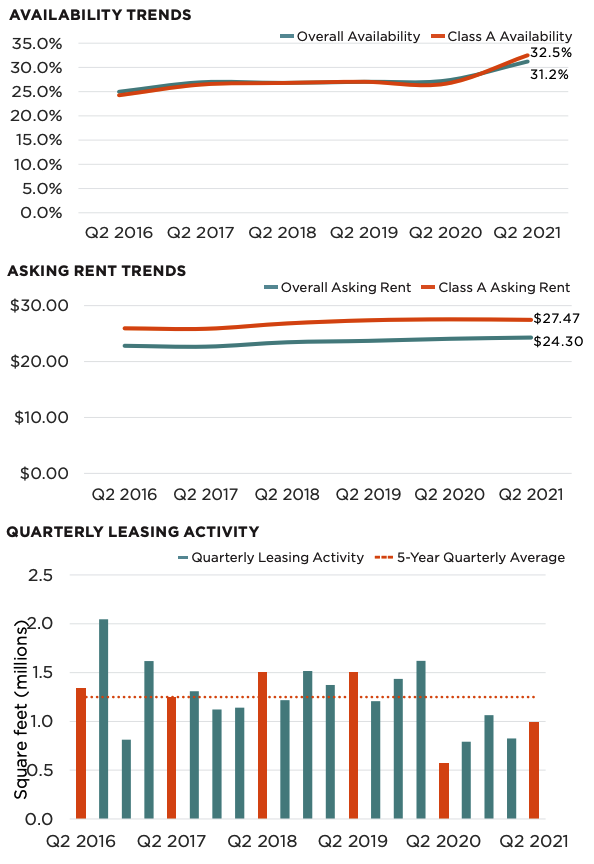

Leasing activity is also down dramatically in both downtown Chicago and the suburbs as compared to previous years, and it’s difficult to say when the metro could return to its pre-pandemic baseline.

However, the flood of available office space both in the city and the suburbs means that office tenants and brokers are still pushing for concessions and generous rent prices. But ultimately, the continued uncertainty surrounding the eventual containment and control of COVID and its variants means that both office property managers and tenant companies have to remain flexible for the time being.

“I think in the conversation, there’s a piece of it that has remained constant is that flexibility is key,” says Eric Feinberg, Vice Chairman and Co-Head for the Chicago region with Savills. “If you’re doing a transaction during the pandemic, you don’t know how much space you’re going to need based on the success or failure of implementing a hybrid workplace model.”

Expansion or contraction options, termination options, and workplace furniture systems are just a few contractual items where flexibility will be crucial, particularly for company heads who are still uncertain about the total amount of needed office space and how it will be utilized, Feinberg adds. And in some ways, flexibility with these terms and options could be viewed as a concession from the office landlord.

“We’re seeing more willingness to provide operational flexibility to the extent that we have not seen before. Any options like this impact the value of a building and impact operations,” Feinberg says of the flexibility in terms such as contraction, expansion and termination. “It’s not easy if you’ve got a bunch of options in the building to manage, so landlords are not always happy to give those, but we’ve seen a lot more willingness.”

Perhaps even more complicated are the rules that each company will implement for its workforce in the office space. Some businesses are increasingly taking a hard line with their staff, mandating that team members get vaccinated or lose their job. But Feinberg suggests that this will remain a tricky situation for office property managers to navigate as each individual business will institute their own guidelines and expectations for employees returning to the office.

But ultimately, Feinberg believes, there will be a return to the office. As other real estate professionals and business leaders have indicated both publicly and to their teams, Feinberg says that are a number of crucial variables that are impacted from being in the office, such as company culture, productivity, mentoring, and the mental separation between personal and professional life.

“In general, there’s more consensus than not that the office is necessary to effectively run a large organization,” he says. “Productivity may have been surprisingly strong over the past 15 months, but I think there’s a doubt that it will be as strong if this lasts 24 or 36 or 48 months with people staying at home.”

But for the moment, we will have to continue to wait and see what happens in the coming quarters. All of the moving parts to the pandemic mean that trends can change week-to-week as businesses and individuals continue to press ahead in work and life, so adaptability and flexibility are more important than ever, Feinberg suggests.

“People can surmise and architects can tell you all day long that this is what the future looks like, but there’s really no black and white answer here. No one really knows what the future actually really has in store, so I think flexibility is key.”

This article also appears in the August 2021 issue of Illinois Real Estate Journal