When evaluating the current state of the Chicago industrial market, a long-term perspective is key, as a rapidly evolving CRE landscape may lead many to a diminished view of what is still a very strong, active market. Compared to 2022, all indicators show a slowdown, but when measured against the mid-2010s, the market is stable and steady.

Chicago’s 1.4 billion-square-foot industrial market grew in 2024, albeit at a slower pace, despite significant headwinds that have slowed activity in most commercial property sectors.

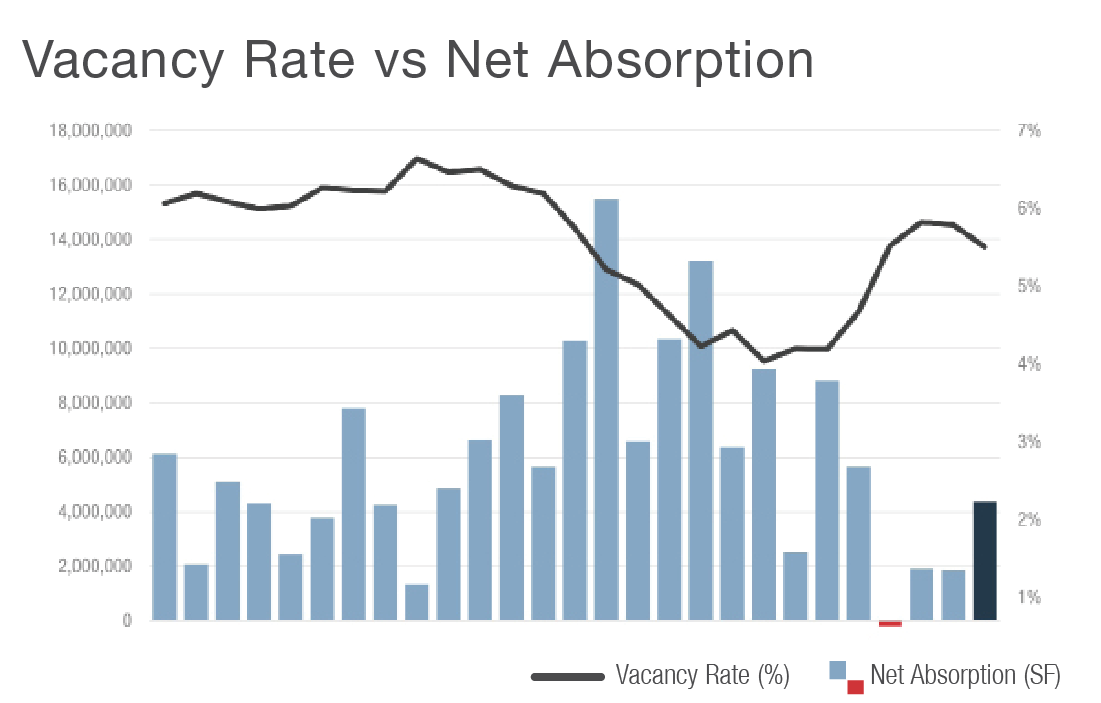

With positive net absorption of 4.4 million square feet during the third quarter and 8.1 million square feet year to date, more space is being occupied than is being vacated. That metric signals a healthy market that may have room for higher lease rates and new inventory in some locations.

Nick Schlanger is director of research services for NAI Hiffman.

Yet over the past two years, the market’s leasing velocity, sales and vacancy rates have reset to a new normal following the feverish pace of speculative building and dealmaking in 2021 and 2022. After a decade of hovering in the 6% range, Chicago-area vacancy rates dipped to 5.1% in 2021 and 4.0% in 2022 amid pandemic-induced supply chain adjustments and e-commerce growth. In fact, 2021 saw a record-high 81.7 million square feet of annual new leasing activity. In response, new speculative development skyrocketed, a trend that has since reversed.

Throughout 2023 and 2024, warehouse demand has cooled, and vacancy rates have crept up as new supply continues to deliver. In response, construction starts have slowed significantly over the past year, which is helping balance supply and demand as this new space gets absorbed.

Chicago-area industrial vacancy was 5.5% at the end of third quarter, down from 5.8% the previous quarter but higher than the 4.7% rate of one year ago, as 24.7 million square feet of new deliveries have come to market over the past 12 months. Leasing activity also slowed, with 5.5 million square feet of new leases signed last quarter, down 50% from the prior three months. Year-to-date new leasing totaled 23.8 million square feet, down nearly 40% from 39.3 million square feet through the same period in 2023.

While the number of leases signed in the third quarter resembles previous quarters at 126, the overall volume is lower because the deals are smaller. A slowing of new big-box industrial deliveries as well as a shift to a more localized approach to shipping and logistics has led to a 20% reduction in average lease size since third-quarter 2023.

New construction declines in 2024

Developers became more conservative over the past year, with only 35.8% of inventory under construction built on a speculative basis, a stark contract from two years ago, when nearly 80% of new projects were spec. Nonetheless, Chicago maintains an active development pipeline, with 15.5 million square feet currently under construction.

During the third quarter, industrial completions in Chicagoland reached 2 million square feet, slightly higher than the 1.3 million square feet during second-quarter 2024 but well short of the 12.4 million square feet delivered during the same period last year.

Industrial demand to increase with reshoring

With still-healthy vacancy and a more sustainable development pipeline, Chicago’s industrial market remains positioned for growth. Adding to its appeal are the market’s centralized location, multimodal transit infrastructure, superior water and power capabilities, and reduced climate risks, all of which will continue to draw major users to the region.

As further evidence of its desirability, Illinois ranked No. 2 in the nation for corporate expansions and relocations for the second year in a row, with 552 expansion or relocation projects in 2023, up from 487 in 2022, according to Site Selection Magazine’s annual ranking.

Onshoring and reshoring activity will only fuel domestic production and manufacturing operations in the quarters ahead, creating further demand for modern industrial facilities that can accommodate such uses. As a result, a year many regarded as a slowdown was actually a gear-up for an extended period of expansion.

For more details and statistics, click here to download the NAI Hiffman Third-Quarter 2024 Industrial Market report.

Nick Schlanger is director of research services for NAI Hiffman.