A quick analysis of recent reports will reflect significant differences between the downtown office market and its suburban counterpart. That said, one thing stands out as consistent across the board: the continued emphasis on tenants’ flight to quality.

To understand these markets better, REjournals turned to two local experts: Colliers Executive Vice President Dougal Jeppe (CBD) and Senior Vice President | Office Advisory Group Jonathon Connor (suburban).

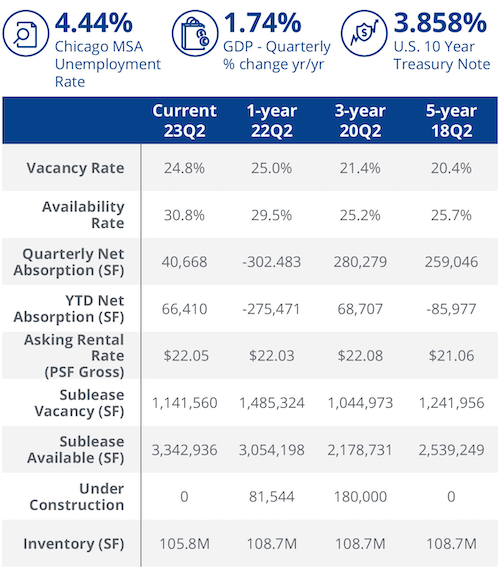

Downtown Chicago/CBD

REjournals: Can you elaborate on the recent increase in available office space in the CBD? What are the primary drivers behind this trend?

Dougal Jeppe: The increase is only about .4% in additional available space from the previous quarter, which equates to about 640,000 square feet. A few large blocks came available in the last quarter (available but still occupied), namely the Molson Coors spaces (132,000 square feet), Katten Muchin (204,000 square feet) Greenberg Traurig (125,000 square feet)

REjournals: Despite the increase in available space, the overall vacancy rate decreased slightly. Can you explain the factors that contributed to this?

Jeppe: The availability is defined as on the market for lease or sublease but still occupied while vacancy is vacant. The vacancy only by about 160,000 square feet or .1% over the last quarter, so not enough of a decrease to equate to any particular factors.

REjournals: The positive net absorption in 2Q23 is a notable shift after 10 quarters of negative activity. Could you provide insights into the types of companies or industries that are driving this positive absorption, particularly in Class A buildings?

Jeppe: Law firms and financial service firms are the most “office forward” industries and are the most active in the market. Although much of the headlines have been about larger firms downsizing, there are many small- to medium-sized firms that are adding bodies and need additional space. There is a limited number of large (50,000 square feet) tenants in the market, so much of the absorption is happening below those size ranges. Additionally, there is consensus continuing to build across all industries that 100% remote work is not productive, so a thoughtful hybrid model is being adopted, thus driving a flight to quality.

REjournals: How are Class B and C assets performing in comparison to Class A buildings in the current market conditions? What strategies are being implemented to address the challenges faced by these asset classes?

Jeppe: If you are given a choice of staying at the Four Seasons or a Hampton Inn, what would you choose? The flight to quality is real and it’s here to stay. If companies are shedding 20-30% of their space, they can afford to stay at the Four Seasons. If the Hampton Inn (i.e., Class B/C) is located near a major tourist attraction, then it will probably do alright because not everyone needs a Four Seasons. The Class B/C that are in the Central and East Loop will be challenged for the foreseeable future.

REjournals: With Chicago office availability reaching a record high of 28% in 2Q23, what are your projections for the remainder of 2023? Do you anticipate further increases in availability and vacancies, or are there factors that may help stabilize the market?

Jeppe: I predict the remainder of 2023 to be about the same. There are fewer developments hitting the market, and the ones that are (i.e., 360 N Green and 225 W Randolph) are attracting the tenants who desire modern amenities in vibrant environments. I think less sublease space will become available, and, in fact, may reverse as some companies rethink their remote strategies. Chicago is a world-class city with access to tremendous talent, a large airport, a diverse population, and a beautiful large body of water. Leaders who travel know this and will choose Chicago as things improve.

Suburban Chicago

REjournals: With tenants seeking high-quality, Class A properties, what specific amenities and features are currently in high demand, and how are landlords responding to these preferences?

Jonathon Connor: Companies are looking to raise the bar with respect to amenity offerings and are looking for amenities that have seen capital investment from landlords and activated common areas to help foster collaboration throughout the building or campus. Examples would be tenant lounges, fresh food offerings, fitness centers and conferencing.

REjournals: The flight to quality in the suburban market seems to be benefiting smaller tenants, as well. Can you elaborate on the advantages they gain from focusing on Class A, spec spaces, and how these spaces meet their unique requirements?

Connor: Spec units allow for tenants to capitalize on the flight-to-quality trend while maintaining flexibility of shorter lease commitments. These programs also provide a convenient, quick and easy solution for small tenants to upgrade their real estate without having to sign a long-term lease or make a significant capital investment.

REjournals: It’s interesting to note that small to midsize tenants are making longer lease agreements in the current market conditions. What factors are influencing their decision to commit to longer lease terms, and how are landlords accommodating their needs?

Connor: Tenants are taking advantage of instability in the market and securing robust concession packages through well-capitalized landlords. The continued escalations of construction costs have also made short-term leases more challenging to complete in instances where significant improvements or modifications are needed to the office space. Longer lease term allows for higher capital investment from the landlord.

REjournals: Multi-tenant inventory reductions through sales for redevelopment are expected to continue. Could you provide examples of the types of properties that are being targeted for redevelopment, and how does this effect the overall leasing dynamics?

Connor: There are several factors that weigh into the potential redevelopment of an office building or site, depending on the potential future use. Location, zoning, size and shape of site, etc. Removal of these assets from the office inventory will slowly reduce the current oversupply of office product in the market. Redevelopment opportunities are found on existing Class B and C office buildings, along with other outdated buildings such as hotels and retail sites.

REjournals: With increased concessions anticipated in the second half of 2023, especially on long-term leases, what are some of the concessions impacting lease negotiations and tenant decisions?

Connor: Capital. Given the high cost to construct and overall cost to relocate office space (furniture and other relocation costs), landlords that are well-capitalized and able to fund transactions will see the most interest from tenants evaluating market options.

REjournals: The vulnerability of landlords with near-term vacancy and maturing debt is an important consideration. What measures are these landlords taking to secure financing for their properties, and how does this influence their leasing strategies?

Connor: With increased interest rates, landlords need to be proactive with their partners to negotiate extensions to loans. Many of the landlords with expiring debt will need to recapitalize, short sale or face foreclosure, as loan extensions will only work for some a small percentage of the market. Increased distress and foreclosures will continue until the market improves.

REjournals: In the current suburban office market landscape, what do you see as the most significant opportunity for tenants and investors?

Connor: Tenants will be able to secure all-time high levels of concession packages with strong landlords who are positioned to fund transactions. Investors who can fund new leasing will likewise be able to take advantage of turmoil with undercapitalized competition.