Bradford Allen, in its Q2/26 Office Market Report: Downtown Chicago and Mid-Year 2026 Office Market Report: Suburban Chicago research reports, found that the downtown Chicago office market showed signs of life in the second quarter, with direct net absorption running in the positive for the first time since 2023 and plans for what may be the market’s first office tower groundbreaking in several years.

Meanwhile, suburban Chicago recorded its strongest first-half net absorption since 2018, with vacancy easing modestly from year-end 2025 levels.

Chicago’s CBD office market posted direct net absorption of 585,646 square feet in the second quarter, a strong improvement from the negative 345,914 square feet recorded in the first quarter. Leasing velocity declined in the first half of the year, with approximately 1.2 million square feet of direct deals completed in the second quarter compared to 1.9 million square feet in the first quarter.

Demand continues to grow for turnkey space. In the CBD, move-in-ready suites accounted for 36.7% of all year-to-date leasing — up from just 20.6% of activity in 2023. Suburban move-in-ready suites accounted for more than half of all deal activity, with over 1 million square feet leased, as tenants increasingly prioritize ease of occupancy amid rising construction costs.

In a significant shift in market sentiment, Sidley Austin announced plans to relocate to 725 Randolph, a new office tower Related Midwest is developing in Fulton Market, with construction expected to begin next year. While Class A vacancy is near historical highs at nearly 22%, there remains intense demand for trophy space due to limited options.

“Chicago’s office market remains in reset mode, but momentum is improving, especially downtown, where developers are regaining confidence and net absorption is, for now, on track to finish the year positive for the first time since 2020,” said Neil Bouhan, senior managing director, research and communications, at Bradford Allen. “Tenants continue to prioritize speed to occupancy and high-quality space, and owners who can deliver that are being rewarded with real leasing traction.”

Downtown Chicago

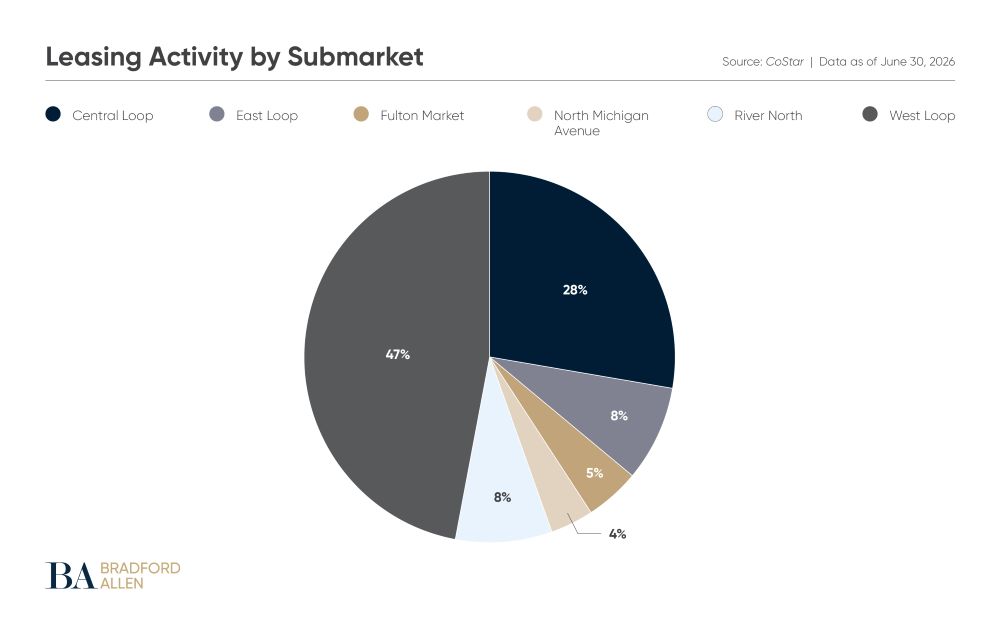

There was positive net absorption in five of six submarkets during the second quarter. Notable leases include Vedder Price’s 163,000-square-foot renewal at 222 N. LaSalle St. and McKinsey & Company’s new 72,113-square-foot sublease at Salesforce Tower. Smaller-footprint activity was prevalent, with just five deals completed above 40,000 square feet and nearly half of all square footage transacted in spaces below that threshold, including Option Clearing Corporation’s new 36,000-square-foot lease at 222 W. Adams St., Hall Prangle’s new 28,827-square-foot lease at 10 S. Riverside Plaza and SAP’s new 28,336-square-foot lease at 333 W. Wacker Drive.

On the investment side, the sale of Citadel’s former headquarters at 131 S. Dearborn St. for $137 million marked the CBD’s highest-priced office deal in more than four years, though it marked a steep discount from the building’s $448 million refinancing in 2020. Other notable transactions included 500 W. Monroe St., which transferred via deed-in-lieu for just under $100 million, a nearly 76% discount from the 2019 purchase price, and the reported $57 million sale of 180 N. LaSalle St., a nearly 70% discount from the $198.5 million acquisition price a decade earlier.

Office-to-residential conversions remain a central response to persistent vacancy, with 25 projects now planned or underway across the CBD. Once completed, these projects will add nearly 4,000 residential units at an estimated total cost of roughly $1.8 billion. A joint venture between Mavrek Development and Acres Capital announced plans in June to convert the 12-story property at 209 W. Jackson Blvd. into roughly 180 apartments, with completion expected in early 2029. Meanwhile, Barings’ redevelopment of 29 S. LaSalle St. hit the market with 211 units and has stabilized at 95% occupancy.

Suburban Chicago

Suburban Chicago’s office market showed continued signs of stabilization in the first half of 2026. The more than 2 million square feet of leased space is a modest increase from the activity during the second half of 2025, while net positive absorption of over half a million square feet marked the strongest first-half performance since 2018.

New leasing drove the majority of activity between January and June, accounting for more than 80% of deals over 10,000 square feet. At approximately 27,000 square feet, the average deal size for new leases this year was 69% higher than the second half of 2025, when the average was 16,000 square feet. Average renewal size, by contrast, shrank to 27,000 square feet from nearly 50,000 square feet in the second half of last year. Notable leasing activity included Inland Real Estate’s new 140,000-square-foot lease at 3050 Highland Parkway in Downers Grove, Takeda Pharmaceuticals’ new 85,000-square-foot lease at Motorola Mobility’s former Libertyville campus and Staples subsidiary Quill’s renewal for nearly 60,000 square feet at 300 Tri State International, with Bradford Allen representing ownership.

Investment activity is on a pace comparable to last year, with $112 million in year-to-date sales volume compared to $235 million traded in all of 2025, but lower than recent history with nearly $740 million transacted in 2022. Pricing, however, moved higher, averaging $131 per square foot year-to-date versus $49 per square foot at the end of last year. Deals included the $86 million sale of 1890 Silver Cross Blvd. in New Lenox to The Landes Group and Farpoint Development, the $23.4 million sale of 1836 Freedom Drive in Naperville and Credit Union 1’s purchase of 450 E. 22nd St. in Lombard for $19.4 million.