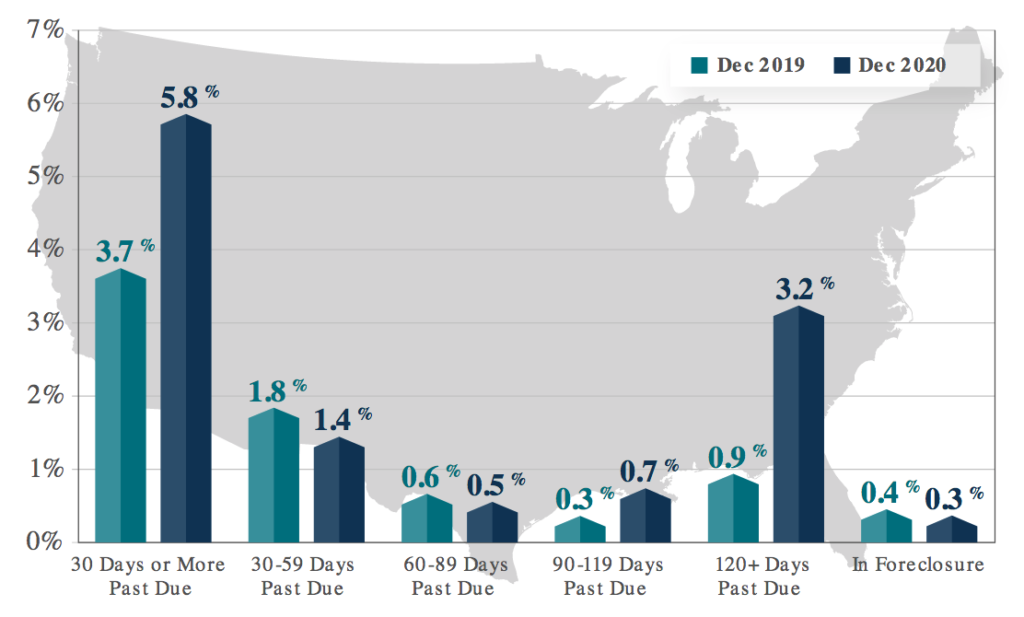

Last year was a very tough one for the American homeowner. According to a recently published report from financial analytics company CoreLogic, every state in the country witnessed an increase in delinquent mortgages. This includes mortgages that are 30 days behind payment and “serious delinquency,” or mortgages that were 90 days or more behind on payment.

Between December 2019 and December 2020, the overall national mortgage delinquency rate increased from 3.7% to 5.8%. Coincidentally, at the beginning of 2020, the country had the lowest delinquency rate on record, the report details. But that rate doubled between March and May last year, going from 3.6% to 7.3%.

The states that were leading the nation in delinquency rate by the end of 2020 were Louisiana at 9.4% overall delinquency, Mississippi at 8.7%, New York with 8.3%, New Jersey at 7.5% and Maryland also at 7.5%.

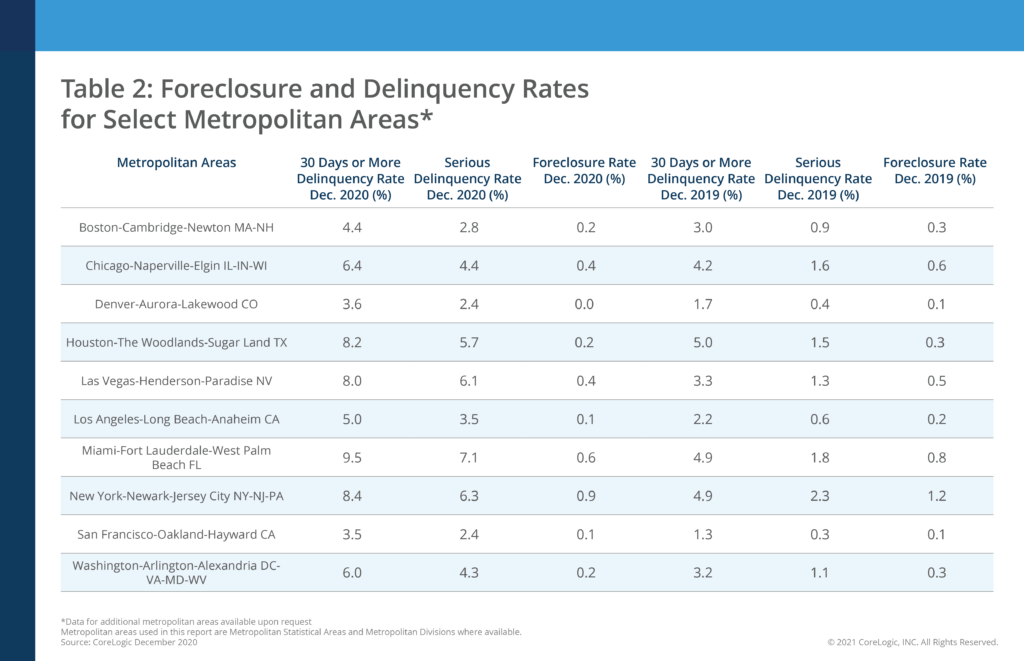

The report also takes a look at ten of the largest metro areas and illustrates their delinquency and foreclosure rates. In the Chicago combined statistical area, aka “Chicagoland,” the delinquency rate (30 days past due) at the end of 2020 was 6.4% while seriously delinquent mortgages were at 4.4%.

Figures for Boston, Denver, Houston, Las Vegas, Los Angeles, and several others were also highlighted in the report.

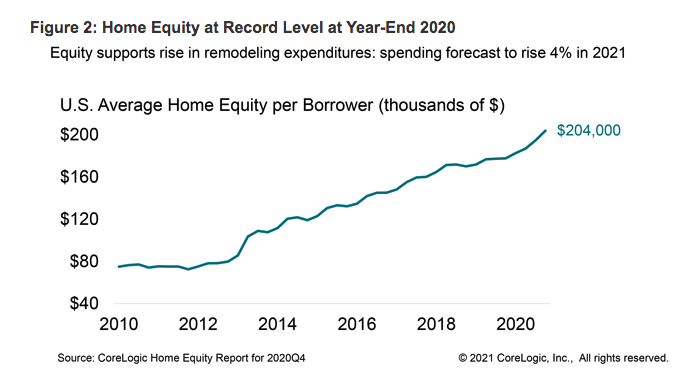

The trend is troubling, no doubt. But the flip side? The total amount of home equity reached a new record by the end of 2020. And with incredibly low inventory and low mortgage rates paired with high demand for housing, prices across many major metros throughout the country have risen steadily in the last year.

According to a separate report from CoreLogic, the average home equity per borrower was over $200,000, and that number was expected to move even higher into 2021. While many homeowners throughout the nation struggled with finances due to mass job losses at the start of the pandemic, those who already had a home equity line of credit (and available room on that line) tapped into that resource to stay afloat during this time.

Another crucial piece of information to note is that while delinquencies have increased dramatically since the beginning of the pandemic, foreclosures are still very low, thanks largely in part to quick action taken at the federal, state and local levels. The number will likely remain low as the Biden administration has extended the national foreclosure moratorium through the end of June.