As a result of growing e-commerce sales, the amount of goods transported through industrial facilities across the country has increased significantly. To capitalize on this growth and remain competitive, companies are modernizing their warehouses to increase operating efficiency and shorten delivery times. Furthermore, many industrial users are looking to automation as a tool to increase efficiency, promote warehouse employee safety and address rising labor costs due to the scarcity of warehouse workers across the country.

In this research paper, we will discuss the cost-benefit tradeoff for automating industrial facilities and why we believe investing in automation is accretive for both landlords and tenants. From a tenant perspective, we believe investing in automation by working with landlords to capitalize the cost of automation within rent expense can be an attractive strategy. This strategy causes a minor increase in a relatively small supply chain cost category (rent and facility costs) in exchange for significant cost savings within much larger supply chain cost categories (primarily labor as well as transportation), which should lead to increased profitability for the company.

From a landlord perspective, we believe investing in automation should result in longer lease terms, higher renewal probabilities at lease expiration and more sustainable intrinsic value for portfolios. From what we have observed, automated facilities are becoming the standard in the current industrial market, and landlords with modern, state-of-the-art industrial facilities will be best positioned to capitalize on long-term rental growth and positive leasing dynamics in the industrial market over the foreseeable future. Moreover, we believe industrial facilities that do not feature automation will be positioned poorly moving forward as more tenants alter their supply chains to focus on automation and the efficiency it provides.

Evolution of the industrial sector

The original industrial environment (20th Century to early 21st Century)

Historically, industrial facilities were constructed as simple boxes with minimal consideration to building specifications such as clear height, building materials, dock doors and parking spaces. These facilities were often constructed to minimize building cost rather than optimize efficiency by using short-sighted design characteristics such as metal construction and a limited number of dock doors. Furthermore, these facilities were generally focused on simply storing goods rather than properly facilitating the movement of goods throughout the facility in an effective manner. As a result of these factors, during the rise of e-commerce sales in the early 21st century, the older Class B and Class C facilities constructed in the 20th century were not well-suited for modern logistics companies seeking to meet rapidly shortening delivery timeframes.

The modern industrial environment (2011-2020)

In 2011, as e-commerce sales began to grow, the industrial market commenced a major shift away from the older industrial facilities described above and toward newly constructed Class A facilities. The chart below summarizes annual construction activity in the U.S. industrial market measured by square feet between 2006 and 2020. The chart demonstrates the significant increase in the construction of new facilities from 2011-2020.

The new facilities constructed from 2011 onwards typically featured modern characteristics such as higher clear height (ranging from 32’-36’+), concrete tilt-up construction, cross dock configuration and more dock doors, among other specifications specifically suited toward fulfilling online orders. However, given e-commerce growth was still in its relative infancy, the facilities constructed earlier in this period were generally designed with one-week delivery expectations.

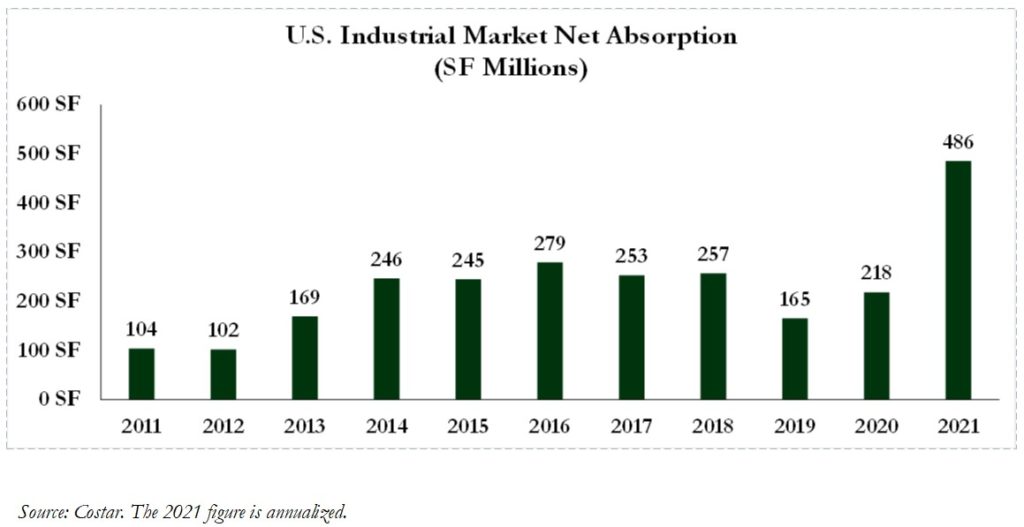

As shown in the table below, the significant level of construction in the industrial sector over this period was coupled with strong leasing fundamentals. From 2014 onwards, net absorption was generally above 200 million square feet on an annual basis (apart from 2019). We believe the strong levels of net absorption despite significant construction activity indicate logistics users are heavily focused on leasing newly constructed, modern facilities to optimize their supply chains for the fulfillment of online orders.

Additionally, occupancy costs represent a small portion of overall supply chain costs for logistics companies, which we believe further motivates tenants to adopt modern supply chains and lease newly constructed facilities. Said differently, the increase in occupancy costs associated with switching from older Class B and Class C facilities to newly constructed Class A facilities is significantly outweighed by the cost savings and increases in efficiency offered by newer facilities.

The new industrial revolution (2021 onwards)

Despite the notable growth in the sector during the last 10 years, we believe that several data points indicate the industrial sector is still primed for significant growth over the foreseeable future. Additionally, we believe that bottlenecks within existing supply chains and growing order volumes are forcing companies to reevaluate their existing infrastructure and identify both areas of improvement and growth opportunities. We believe this combination of growth and a need to overhaul and expand existing supply chain infrastructure will drive a new shift in the industrial sector. This shift will involve logistics companies working with landlords to build out highly automated, state-of-the-art industrial facilities that are better suited to meet the demands of the modern logistics environment.

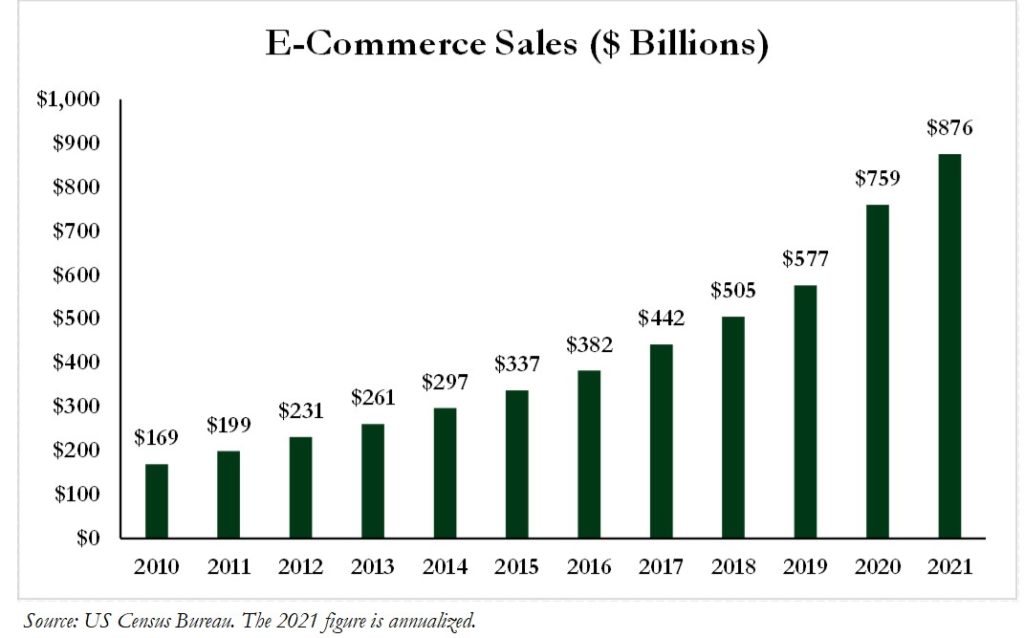

E-commerce sales have grown materially over the last two years, which we believe will drive additional growth in the industrial sector. As shown in the chart below, in 2019, e-commerce sales were $577 billion, and e-commerce sales are currently projected to reach $876 billion in 2021. To put that level of growth in perspective, the approximately $300 billion of additional online sales seen over two years are equivalent to all of the growth experienced from the six-year period between 2013 to 2019.

Additionally, according to the US Census Bureau, e-commerce sales comprised approximately 13% of total U.S. retail sales as of Q2 2021. Thus, we believe there is significant runway left for future e-commerce sales growth, which should result in continued demand growth for industrial facilities. This expectation is further solidified by the sector being on track for record net absorption in 2021 (annualized 2021 absorption is 486 million square feet as shown in the chart on the previous page).

Coupled with consumers’ increased e-commerce purchases, we believe there is a confluence of trends in the industrial sector that indicate a significant investment in automation by tenants and landlords is highly likely. These trends include continued e-commerce sales growth, a shift toward same-day delivery and a severe labor shortage in the industrial sector.

In particular, while industrial facilities constructed over the last 10 years offer an immense improvement over obsolete facilities constructed prior to 2000, we believe they are not fully optimized to allow companies to meet growing order volumes while solving for same-day delivery and mitigating the impact of the current labor shortage. In the following section, we will discuss how automation offers a potential solution for logistics companies to address all of these issues.

Automation’s value proposition

Within this section, we will further discuss how investment in automation can potentially solve two key issues for logistics companies.

Shortens delivery times

When e-commerce was in its infancy, delivery times between one and two weeks were considered adequate. However, as e-commerce sales have grown significantly, competition among e-commerce companies to reduce delivery times has intensified. Currently, consumers are demanding one to two-day delivery windows, and in some cases have become accustomed to same-day delivery. As a result, existing industrial facilities that previously supported one to two-week deliveries are becoming obsolete. Moreover, to execute the “ship to shore, shore to door” process in a manner that allows for same-day delivery, significant portions of the existing industrial footprint need to be replaced with modern industrial assets.

As a result, companies in the logistics industry are looking to increase efficiency and order accuracy to shorten delivery times, and many online retailers have looked to automation as a solution. Without automation, order pickers typically spend 70%-75% of their time traveling throughout the warehouse to pick items for packaging. With a well-implemented robotics-based goods-to-person automation system, warehouse picking times can be reduced by 60%-70%. The reduction in picking times allows goods to be packaged and loaded into trucks in a more expeditious manner, better positioning companies to achieve same-day delivery.

Additionally, not only does warehouse automation allow warehouse associates to be efficient with time, it also allows for increased efficiency in warehouse space. According to Prologis, warehouse automation can increase revenue per SF of warehouse space by 10%-20%. This increased level of throughput results in more goods moving through warehouses on a daily basis, which helps companies capitalize on growing e-commerce sales while shortening delivery times.

Solves labor shortage

In August, U.S. warehouse employment hit an all-time high of 1.47 million according to the Bureau of Labor Statistics. August also marked the fourth consecutive month that the sector has seen a rise in employment. As more companies build out their logistics footprints to meet rising e-commerce demand, warehouse workers have become increasingly scarce.

In a survey conducted by MHI and Deloitte Consulting, 65% of supply chain firms polled cited hiring qualified workers as a top company challenge. For example, in FedEx’s Q4 2021 earnings call, the company’s COO, Raj Subramaniam, said, “The inability to hire team members, particularly package handlers, has driven wage rates higher and creates inefficiency in our networks as we use overtime to cover open shifts and route volume around known constraints just as a few examples.”

Amazon is also seeing an increase in competition for warehouse workers. In the company’s Q2 2021 earnings call, CFO Brian Olsavsky said, “It’s a very competitive labor market out there and certainly, the biggest contributor to inflationary pressures that we’re seeing in the business.” As demand for warehouse workers rises, wages have felt upward pressure, and many companies have looked to warehouse automation as a potential solution.

Warehouse automation provides companies with an opportunity to optimize labor costs by increasing the productivity of full-time employees in warehouses. Additionally, the lack of available warehouse workers is inhibiting companies from fully capitalizing on growing e-commerce sales. Thus, automation not only allows companies to optimize labor costs, it also eases a major bottleneck in expanding supply chains.

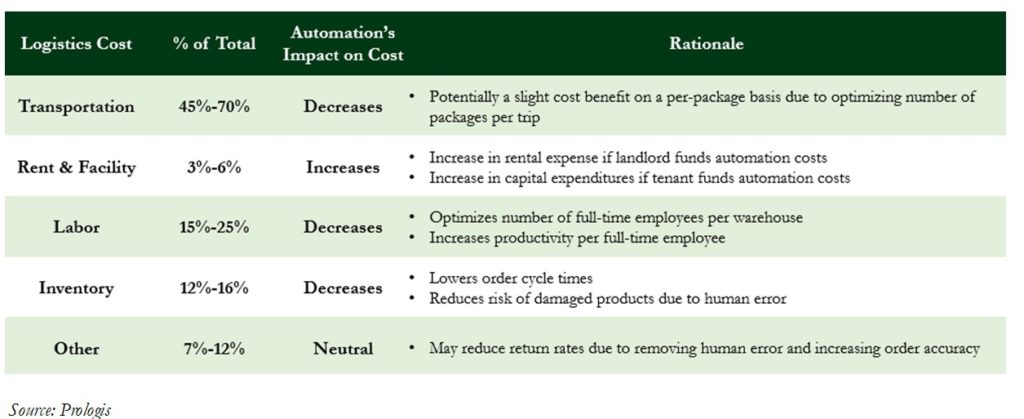

The size of labor costs relative to occupancy costs for logistics companies further supports investment in automation. Labor represents one of the largest cost categories for companies in the logistics industry (approximately 15%-25%), while rent and facility costs make up a relatively small portion of overall logistics costs (approximately 3%-6%). Thus, automation offers logistics companies an opportunity to mitigate cost growth in a large category (labor cost) in exchange for a relatively immaterial increase in a small cost category (rent & facility costs). As a result, paying higher occupancy costs for automated facilities should offer significant net cost savings for logistics companies.

The table below summarizes the value proposition of automation within the wider context of overall supply chain costs. In addition to the labor cost savings discussed above, automation likely optimizes the cost structure and efficiency for other large categories such as transportation and inventory, which combined represent about 65%-70% of total costs. For example, automation may potentially lower transportation costs by decreasing loading times and increasing the number of packages per truckload. Additional examples are provided below.

Logistics experts confirm focus on automation

We believe a subset of companies in the logistics industry are at the forefront of a long-term shift away from older industrial facilities and towards newly constructed, state-of-the-art facilities that feature automation. Two prominent tenants represent this movement in their recent facilities.

GXO Logistics

GXO logistics is a leading third-party logistics provider that provides supply chain solutions to a range of companies spanning multiple sectors. GXO has set itself apart from its competitors by investing in automation to drive productivity benefits that competitors cannot often provide.

In regard to warehouse automation, XPO’s Chief Strategy Officer (GXO spun off of XPO this year), Matt Fassler, said, “We have lots of very compelling opportunities to introduce advanced automation and robotics. It’s one of the things that our customers are looking to us for. It’s one of the big drivers of outsourcing and contract logistics that ties in very well with e-commerce and omnichannel retail.”

As an example of its automation strategy, GXO has a partnership with GreyOrange Pte. Ltd, a robotics manufacturer. GreyOrange’s robots can lift from 1,000 to 3,500 pounds and allow associates to fulfill 48 orders simultaneously. In regard to increased demand as a result of the robotics strategy, Malcom Wilson, CEO of GXO, said, “We can all relate to this: right now, order-fulfillment times are being compressed. What used to be a five-day logistics process is now down to one day or less. Advanced automation and intelligent machines are cost-effective ways to meet these expectations.”

According to GXO’s CIO, Sandeep Sakharkar, automation allows goods to move through its supply chain in half the time it takes without robotics.

Amazon

Amazon has historically been a strong proponent of warehouse automation to increase productivity. In 2012, the company acquired Kiva Systems, a leading warehouse robotics manufacturer, for $775 million. Kiva, later renamed Amazon Robotics, produces robots that provide significant efficiencies in the picking process. Prior to the use of automation, in order to ship an item, a warehouse associate would retrieve the item from a storage rack in the warehouse using a forklift, return to the boxing area to box the item and then label the box to be shipped.

Kiva’s robotics expedite the picking process. When an order is registered in the system, the nearest Kiva robot will retrieve the item from its designated area or pod in the warehouse and transport it to an Amazon associate for labeling and boxing. Amazon has significantly increased its investment in robotics as shown by Kiva’s growth over the last several years. In 2014, Amazon operated with approximately 15,000 warehouse robots while, last year, Amazon operated more than 200,000 Kiva robots across its global network of warehouses.

Robotics are also key to Amazon’s focus on promoting worker safety. In May, Amazon announced a goal of reducing recordable warehouse incident rates by 50% by the year 2025. Kiva robots not only increase productivity (they can increase associate picking capacity from 100 to 300 per hour), they can also help Amazon associates stay safe in the warehouse by completing more dangerous tasks traditionally completed by associates.

Automation’s impact on industrial real estate

Growth in construction costs

We believe automated facilities will become the standard in the industrial market as logistics companies look to capitalize on growing e-commerce sales and solve issues related to labor shortages and compressing delivery timeframes. As a result, we expect landlords to increasingly incorporate the cost of building out automation into construction budgets for new industrial facilities, which will inherently cause an increase in construction costs and prices for industrial facilities.

With that said, we believe landlords will be compensated for this additional investment through 1) an ability to charge higher rental rates 2) longer lease terms and higher renewal probabilities and 3) increased long-term intrinsic values, all of which are discussed in more detail below and on the following pages.

Growth in industrial rental rates

As shown in the chart below, the industrial sector has experienced strong rental growth over the last decade due to the supply and demand imbalance in the sector. We believe this historical trend offers two primary insights. First, logistics companies are generally willing to pay higher rental rates to expand their supply chains and capitalize on growing e-commerce sales during periods of growth. We believe this concept is intuitive considering the small relative size of occupancy costs compared to other supply chain costs such as labor and transportation. As a result, logistics companies, such as FedEx, Amazon and GXO, are heavily incentivized to pay higher rental rates for newly constructed, Class A real estate assets that drive cost savings, increased efficiency and higher throughput.

Second, the supply of industrial real estate cannot typically keep up with demand during periods of elevated growth. Despite the significant demand in the industrial sector, there are a variety of constraints that limit supply growth on an annual basis such as the time required to complete processes like permitting and entitlement, the scarcity of well located sites, and related factors. We believe these two insights, in combination with the expectation for continued growth in e-commerce sales, position the sector for continued rental growth moving forward. The 7.6% annualized rental growth through 2021 supports this conclusion.

Looking more specifically at the impact of automation, we believe newly constructed, state-of-the-art facilities that feature automation will be best positioned to capitalize on this upcoming period of rental growth. Furthermore, we believe landlords with facilities that feature automation will be able to garner a rental rate premium over less sophisticated facilities. Historical rental growth trends and continually positive net absorption during periods with significant construction activity indicate industrial tenants have a willingness to accept higher rental rates in exchange for the increased operating efficiencies offered by new facilities.

Looking forward, we believe automation will provide significant advancements in operating efficiency for logistics companies similar to the improvements that occurred when industrial facilities started implementing concrete tilt-up construction, cross-dock designs, additional dock doors, and related features. Thus, landlords that invest in automation will not only benefit from the secular growth in industrial rates, they will likely be able to charge a premium over less sophisticated industrial facilities as a result of offering more operating efficiencies to tenants through lower labor costs and increased throughput.

Longer lease terms and higher renewal rates

We believe automated facilities will become the standard in the industrial sector, and the offering of increased operating efficiency will result in long-term occupancy at these facilities. We expect automated facilities to garner longer lease terms as well as higher renewal probabilities at lease expiration. According to Prologis, tenants that are significant energy consumers due to automation features at their properties, execute leases that are on average more than 50% longer than the typical logistics occupier.

Prologis also reported that several tenants are exploring automation investments to increase site productivity, which we believe would prevent them from relocating, translating to higher retention rates. Thus, as competition amongst logistics companies intensifies, we believe tenants will likely be willing to sign longer leases for modern facilities that feature automation and allow them to lower labor costs and improve operational efficiencies within their supply chains.

Additionally, we believe the focus on last mile facilities will also increase tenant demand for automated industrial facilities, which in turn should increase renewal probabilities given the footprint of last mile facilities is constrained by the lack of available land in densely populated areas. With limited supply of infill logistics space in densely populated areas, warehouse users are seeking to maximize warehouse efficiency, which can be accomplished through increased levels of automation.

Automation offers long-term intrinsic value

As the industrial sector shifts toward automated facilities, we believe tenants will heavily favor new facilities that feature automation versus less sophisticated alternatives. We believe this conclusion is well supported by historical trends in the industrial market, the relative size of occupancy costs versus larger supply chain cost categories and the current issues in the industrial market such as labor constraints and compressing delivery times. As a result of the increased preference by tenants for automated facilities, we believe pricing discrepancies will occur in the market as investors underwrite lower renewal probabilities and rental rates for facilities that do not feature automation. Thus, by investing in automation, we believe landlords will benefit from owning assets that should feature more sustainable intrinsic value.

Conclusion

We believe the industrial market is currently in the early stages of a long-term shift towards building, owning and leasing highly sophisticated industrial facilities that feature automation. Moving forward, we expect tenants to primarily focus their supply chain expansions on leasing state-of-the-art, Class A industrial facilities that feature the built-in infrastructure needed for significant interior automation. We believe a focus on automated facilities will provide tenants with several benefits including 1) increased efficiency and shorter delivery times 2) lower overall supply chain costs as the increase in occupancy costs will be offset by the savings in labor and transportation costs 3) an ability to grow throughput levels despite the scarcity in labor markets and 4) improvements in safety for warehouse associates. Thus, we expect tenants to view investments in automation as a highly beneficial cost-benefit tradeoff due to increases in both efficiency and profitability.

From a landlord perspective, we believe investing in automation for industrial facilities also offers an attractive cost-benefit tradeoff. We see investments in automation leading to longer lease terms, higher renewal probabilities at lease expiration and more sustainable intrinsic value relative to non-automated facilities. Moreover, we believe automated facilities are becoming the standard for tenants in the modern industrial market, and older properties lacking the core components of automated facilities will eventually become obsolete.

Taking these factors together, we believe the industrial distribution market, as a whole, is well positioned for significant rental growth and positive leasing fundamentals over the foreseeable future. However, for the reasons described above, we believe automated facilities are best positioned to capitalize on these positive fundamentals. As a result, we believe developers and landlords should increasingly consider incorporating the cost of automation within construction budgets for new industrial facilities to best position their portfolios to sustain long-term intrinsic value.

Appendix: Examples of automation in industrial facilities

Warehouse automation explained

Warehouse automation is focused on improving efficiency and accuracy within industrial facilities. When implemented correctly, automated facilities can be more productive, safe and cost efficient compared to older industrial facilities. Warehouse automation is often utilized to improve the following logistics operations: inventory management, unloading, receiving, storage, picking, packing, loading and shipping. Historically, these tasks have been completed through warehouse employee labor who utilize equipment such as racks, pallet jacks, and forklifts. Going forward, many of these functions will likely be accomplished through both the digital and physical forms of warehouse automation as defined in more detail below.

Digital automation

Digital automation focuses on taking manual processes, like inventory management, and automating them through the use of a software system. The primary benefits of digital automation include enhanced security, data management efficiencies, reduced operational risks, reduced manual processes and human errors. Common elements of digital automation can include using tablets/smartphones, wireless barcode scanners, software networks, cloud databases, and data analytics platforms.

Physical automation

The earliest version of physical automation was the assembly line. Since then, physical automation tools have become significantly more advanced due to the introduction of artificial intelligence, which is commonly used within advanced warehouses through the implementation of robotics. Physical automation can generally be grouped into the following two categories:

1) Fixed automation: Fixed automation is the use of specialized equipment to create an efficient process for assembly. These systems are utilized in warehouses with high-volume needs as they reduce the need for time-consuming tasks handled by associates. As a result, businesses that utilize fixed automation can quickly streamline their operations. Common examples of fixed automation include: conveyor belts, automatic sorters, robotic palletizers, and vertical lifts.

2) Mobile automation: Mobile automation systems include goods-to-person (GTP) technology, autonomous mobile robots (AMRs), and automated guided vehicles (AGVs). GTP technology involves the use of robotics or machines that bring materials to workers for assembly or packing (cranes or conveyors). AMRs are utilized to move goods throughout a warehouse and use navigation systems to create routes that improve efficiency and safety. AGVs are material handling systems or load carriers that travel autonomously throughout a warehouse without an operator or driver (automated forklifts or carts).

MaCauley Studdard is managing director, Austin Davis, associate, and Mark Clinton, associate, with St. Louis-based ElmTree Funds, LLC. You can reach ElmTree at 314-828-4200 or online at www.elmtreefunds.com.

Disclaimer

This newsletter is not an offer to sell, or a solicitation of any offer to buy, any security. Any such offering may be made only by an offering memorandum that would be furnished to prospective investors who express an interest in an investment program of the type being considered, and that would describe the risks associated with an investment in the investment program. The information is provided to you as of the dates indicated and ElmTree Funds, LLC does not intend to update the information after its distribution, even in the event that the information becomes materially inaccurate. The information contained herein is confidential and may not be reproduced in whole or in part nor disclosed by the recipient to any other party without our prior written consent. Nothing contained herein should be construed as legal, business or tax advice.